Evaluation of the Expanding Market Opportunities (EMO) Program

Audit and Evaluation Branch

Natural Resources Canada

FINAL REPORT – December 30, 2019

Table of Contents

- EXECUTIVE SUMMARY

- INTRODUCTION

- FINDINGS: RELEVANCE

- FINDINGS: EFFECTIVENESS

- FINDINGS: EFFICIENCY

- CONCLUSIONS

- APPENDIX 1 EVALUATION TEAM

- APPENDIX 2 LIST OF KEY DOCUMENTS REFERENCED IN REPORT

- APPENDIX 3 STATUS OF MANAGEMENT ACTIONS IN RESPONSE TO PAST RECOMMENDATIONS

List of Acronyms

- AEB

- Audit and Evaluation Branch

- BC FII

- British Columbia Forestry Innovation Investment

- CBFA

- Canadian Boreal Forest Agreement

- CFS

- Canadian Forest Service

- CLT

- Cross-Laminated Timber

- CWG

- Canada Wood Group

- EMO

- Expanding Market Opportunities

- FMS

- Funding Management System

- GBA+

- Gender-Based Analysis Plus

- GCWood

- Green Construction through Wood

- GHG

- Greenhouse Gas

- NBCC

- National Building Code of Canada

- NRCan

- Natural Resources Canada

- R+D

- Research and development

- SLAP

- Softwood Lumber Action Plan

- SME

- Small- and Medium-sized Enterprise

- TWBDI

- Tall Wood Building Demonstration Initiative

Executive Summary

About the Evaluation

This report presents the findings, conclusions, and recommendations from the evaluation of the Canadian Forest Service’s Expanding Market Opportunities (EMO) program. The objective of this program is to expand international markets for Canadian forest products and promote increased wood use in North American non-residential and mid-rise construction. The evaluation covers the period from 2015-16 to 2018-19. Actual expenditures for the program over this period were approximately $69 million.

The objective of the evaluation was to assess the relevance, effectiveness and efficiency of the EMO program. The evaluation focused on the impact that changes in context and delivery may have had on program effectiveness or efficiency since the last audit and evaluation were completed in 2016, including the extent to which management actions in response to previous recommendations had been effectively implemented. Results of this follow-up are summarized in Appendix 3.

This program is a component of NRCan’s Forest Sector Competitiveness Program, which also includes a suite of forest sector innovation programs. More information on the relevance and performance of these programs is found in the Evaluation of Forest Sector Innovation Programs (2019).

What the Evaluation Found

Relevance

Overall, the evaluation found that the Expanding Market Opportunities program continues to be relevant and well aligned with federal government and NRCan roles, responsibilities and priorities. The EMO program is also generally aligned with the needs of the forest sector. However, specific needs differ among various segments of the forest industry and regions of Canada. While the EMO program has recently made efforts to address these differing needs, in many cases it is still too soon to know the results. While it is also of increasing importance to support the growth of the bioeconomy, we found that there are barriers to effective engagement with the nascent bioproducts sector.

Effectiveness

We found that the Expanding Market Opportunities program has been responsive to factors affecting its ability to achieve its intended outcomes and operate with efficiency, including global competition and market volatility. The program demonstrates a strategic approach to identifying and pursuing opportunities for market diversification. Moving forward, it will be important to ensure that these international activities remain aligned with NRCan’s broader strategic framework for international activities and new International Departmental Plan.

While market diversification requires years of sustained effort, there is evidence of continued progress towards achievement of the program’s intended outcomes. The EMO program is effectively addressing regulatory, environmental and technical barriers to international market access. There has also been increased awareness of wood products and construction technologies among end users. While some related corporate targets were not met over the evaluation period, the long-term trend shows clear indications of progress in key target markets.

Domestically, the program’s support for technical research and testing has contributed to amendments to building codes, creating an enabling environment for increased wood use in non-residential and mid-rise construction. This uptake has been effectively supported by information, education and capacity building. Corporate targets to increase the dollar value of wood products used in domestic non-residential construction projects were exceeded. Further efforts towards broader domestic adoption and commercialization of wood in construction could be facilitated by increasing the program’s reach to new target audiences.

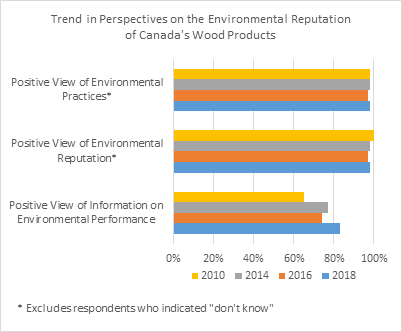

Program activities also continue to result in achievement of expected outcomes for Canada’s environmental reputation. Canada’s strong brand as an environmentally responsible choice gives it a competitive advantage in international markets. However, Canada’s reputation for sustainable forest management is less well regarded domestically. Better communication of the forest industry’s environmental performance and wood’s environmental benefits within Canada could support domestic marketing of wood as a preferred option for sustainable construction.

Efficiency

We found that the EMO program continues to be delivered in an efficient and economical way. Changes in the program’s expenditure profile over the evaluation period align with increased funding levels and revisions made to cost-share requirements. While stakeholders have mixed perceptions on the appropriateness of the revised cost-share structure, evidence indicates that the EMO program was somewhat more effective at leveraging funds through this evaluation period than the previous. Additional changes in program design and delivery – such as a new management structure for the program’s North American Markets component – have positively impacted both program efficiency and effectiveness.

However, we also found that issues with program efficiency and economy raised during the previous evaluation have yet to be fully resolved. Principal among these, the need for continual program renewal hinders its efficiency. Given that market transformation requires years of sustained effort, program efficiency requires sustainable funding levels allocated over an extended period.

Opportunities also exist to significantly strengthen and streamline the EMO program’s performance measurement system. These revisions should include integration of considerations for gender-based analysis to ensure that the program collects the information it needs to support efforts aimed at increasing equity and diversity in the forest sector.

Recommendations and Management Response

| Recommendation | Management Response |

|---|---|

| 1. The Canadian Forest Service should work with partners to address gaps in market research identified by the evaluation and program stakeholders, including developing forward insights into market opportunities for new bioproducts. | Agreed. The Canadian Forest Service will consult with partners to identify and address gaps in the program’s current suite of market studies and strategies, including the market development needs of the emerging bioproducts sector. Due date: March 2023. |

| 2. The Canadian Forest Service should review its pilot of in-market infrastructure in the Middle East, ensuring that it is aligned with NRCan’s broader international strategy. CFS should also share its lessons learned from this review so as to inform NRCan’s implementation of similar positions in other sectors. | Agreed. In April 2019 the Canadian Forest Service contracted with a consulting firm specializing in evaluation and performance management to perform an impact assessment of the pilot in-market infrastructure in the Middle East. Lessons learned will inform the future of the pilot and be shared within the department at the Directors General International Affairs Committee. Due date: March 2020. |

| 3. The Canadian Forest Service should work with domestic partners to extend outreach to new target audiences in the delivery of the North American Markets component, including considerations for more innovative use of online media. | Agreed. The Canadian Forest Service will work with domestic partners to increase engagement with different target groups in the delivery of the North American Markets component. This includes launching new education programs with insurers, information campaigns on the implications of the 2020 National Building Code, and investing in enhancements to the Think Wood online communications platform as well as those of other industry stakeholders. Due date: May 2020. |

| 4. The Canadian Forest Service should work with partners to increase communication of the forest industry’s environmental performance within Canada and the domestic marketing of wood as a preferred option for sustainable construction. | Agreed. The Canadian Forest Service will work with partners to improve communication of the forest industry’s environmental performance within Canada and the domestic marketing of wood as a preferred option for sustainable construction. The program will partner with industry on a National Sustainability Coordinator position at the Canadian Wood Council that will increase awareness and reduce/remove barriers and misinformation related to wood use in sustainable construction, and to position wood as the building material of choice, based on science. Due date: May 2020. |

| 5. The Canadian Forest Service should strengthen and streamline the EMO program’s performance measurement system, to reduce reporting burden and improve clarity of its performance story. This should include integration of GBA+ considerations in data collection. | Agreed. Work is underway to strengthen and streamline the performance measurement system and performance metrics, including GBA+ considerations, as part of the renewal efforts of Budget 2019. Due date: March 2020. |

Introduction

This report presents the findings, conclusions, and recommendations from the evaluation of the Canadian Forest Service’s (CFS) Expanding Market Opportunities (EMO) program. The evaluation examines the period from 2015-16 to 2018-19. Natural Resources Canada’s (NRCan) Audit and Evaluation Branch (AEB) undertook the evaluation between November 2018 and June 2019. It was conducted in accordance with the Treasury Board Policy on Results (2016), Section 42.1 of the Financial Administration Act and in response to a Treasury Board commitment to evaluate the program by March 2020.

Budget 2019 proposes an investment of up to $64 million over three years for the continued delivery of the Expanding Market Opportunities program. Results of the evaluation will help inform requests for program renewal.

Program Information

The Canadian Forest Service has been operating the Expanding Market Opportunities program in its current form since 2012. This program brings together a number of earlier programs designed to expand offshore markets for Canadian forest products and promote increased wood use in North American non-residential and mid-rise construction that were created between 2002 and 2007. Within the Departmental Results Framework, the program is currently a component of the Forest Sector Competitiveness Program (Program 3.1) under NRCan’s Core Responsibility for Globally Competitive Natural Resource Sectors.

This contribution program was most recently renewed in June 2017 under the Softwood Lumber Action Plan, which provided the program with $45 million in new funding over three years (2017-18 to 2019-20). Total planned expenditures over the period of evaluation were $69 million.

The objective of the Expanding Market Opportunities program is to increase market opportunities for the Canadian forest industry, both in terms of the diversification of export markets and of international and domestic market segments. The program includes two components:

- The Offshore Markets Component seeks to expand the export opportunities of Canadian wood producers by cost-sharing international market access and development activities with forest industry associations and other stakeholders. This includes support to: (a) maintain and expand a network of offices and forest industry staff located in offshore markets; (b) increase the wood product knowledge of end-users (e.g., consumers, builders and architects); and (c) address international market access and regulatory issues that could limit trade in Canadian forest products through technical support and promotion of the Canadian forest sector’s environmental performance. While focused on the wood products used in building applications, this component applies to wood products used in a wide variety of end uses.

- The North American Markets Component builds capacity to increase the use of wood in non-residential and mid-rise construction in Canada by cost-sharing activities for the generation and dissemination of knowledge needed by end-users. This includes support to: (a) maintain a network of offices and technical advisers located in targeted Canadian provinces; (b) develop and disseminate technical information; and (c) conduct technology transfer and training.

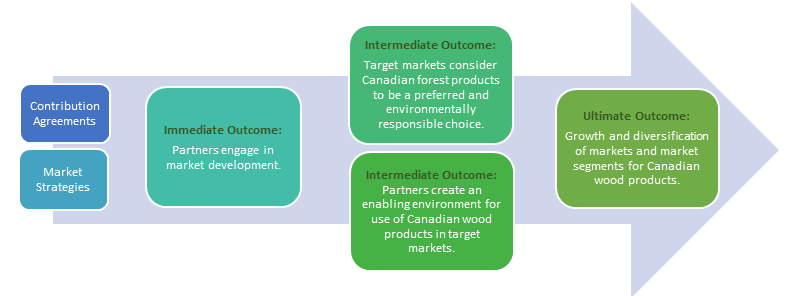

The following presents a simplified logic model for the Expanding Market Opportunities program developed for the purposes of this evaluation. Key elements in this logic model are derived from the program’s existing performance measurement system.

Text version

Description: A simplified logic model for the Expanding Market Opportunities program. The two outputs are “contribution agreements” and “market strategies”. These lead to the immediate outcome that “partners engage in market development.” This in turn leads to two intermediate outcomes. First, that “target markets consider Canadian forest products to be a preferred and environmentally responsible choice,” and second that “partners create an enabling environment for use of Canadian wood products in target markets.” The ultimate outcome is “growth and diversification of markets and market segments for Canadian wood products.”

Program Governance

This program is under the responsibility of the Director General of the Trade, Economics and Industry Branch who reports to the Assistant Deputy Minister of NRCan’s Canadian Forest Service. The program is managed by the Director, Trade and International Affairs Division. These senior representatives provide strategic advice and guidance on the management and delivery of the Expanding Market Opportunities program. They are supported by a team within NRCan that is responsible for the administration of the program.

An evaluation committee offers advice to this team on program outcomes and priorities and participates in the evaluation of submitted applications for funding. Membership on this committee includes a mix of representatives from the federal government (e.g., NRCan and Global Affairs Canada), provincial governments and industry.

Cost-Share and Delivery Partners

The EMO program’s success stems from years of successful partnerships with industry and provinces, including collaborative funding arrangements. Eligible cost-share recipients include forest products associations, manufactured housing associations, provinces and provincial Crown Corporations, and organizations engaged in forest product research.

Wherever possible, initiatives are delivered jointly on behalf of the Canadian forest industry. While not the only industry association engaged with the program, most projects in the Offshore Markets component are coordinated through the Canada Wood Group (representing eight major Canadian wood products associations). Most work under the North American Markets component is delivered through the Canadian Wood Council (a national federation of Canadian wood products associations).

Similarly, while also engaged with other provinces, the EMO program has harmonized its delivery with the Market Initiatives Program delivered by the Government of British Columbia's Forestry Innovation Investment (BC FII), a market development agency for provincial forest products.

Text version

Infographic showing the four categories of eligible cost-share recipients: forest products associations; manufactured housing associations; provinces and provincial Crown corporations; and organizations engaged in forest product research.

Evaluation objectives and methods

This evaluation examines the period from 2015-16 to 2018-19. The last evaluation and audit of the Expanding Market Opportunities program were both completed in 2016, covering the period 2010-11 to 2014-15 and 2012-13 to 2015-16 respectively. Overall, these projects found that the program was relevant, well-managed and delivering expected results. Given these positive results, the purpose of the current evaluation was to:

- Confirm ongoing program relevance and performance;

- Review changes in context and delivery (including consideration of gender-based analysis), and the impact that these changes may have on program effectiveness or efficiency; and

- Identify the impact of management actions in response to past recommendations.

| Document Review | Literature Review | Database and File Review | Key Informant Interviews |

|---|---|---|---|

| A review of program documents, as well as NRCan and federal government strategic and corporate documents. This line of evidence informed findings across all questions of the evaluation. |

A review of published literature, with a focus on emerging issues and best practices in forest products market access and diversification. | A review of project-specific financial and results data contained in the EMO program’s Funding Management System (i.e., proposal and reporting management tool and project database). | Thirty-nine (39) interviews with stakeholders including the EMO program’s management and staff, and external stakeholders such as provincial governments, industry associations, and other federal departments and agencies. These interviews were used to obtain perspectives on program relevance and performance. |

Evaluation limitations and mitigation strategies

The evaluation used multiple lines of evidence in order to mitigate against any limitations associated with individual methods. This enabled the triangulation of evidence across sources of information to identify valid findings and conclusions relative to the evaluation questions. Nevertheless, the following limitations should be considered when reviewing the findings from this evaluation:

- The evaluation’s scope and approach were calibrated in recognition of the relatively short period elapsed since the completion of the previous audit and evaluation. As such, the evaluation expended less effort in examining areas where there have been no or few known changes to the programming context (e.g., government roles and responsibilities).

- We consider the views of key stakeholders to be well represented in our analysis. However, given the evaluation’s calibrated approach, we did not obtain the perspectives of beneficiaries located in offshore markets or end-users of forest products. Where available, we mitigated this limitation by considering secondary evidence provided by the EMO program or its proponents.

- Particularly related to program effectiveness, the evaluation relies heavily on secondary data provided by the EMO program and its proponents. The evaluation team has not independently verified this data. Areas where there may be specific concerns with data reliability are identified where relevant in the report.

What We Found

Relevance

To what extent is there a continued need for the program?

To what extent is the program aligned with federal government and NRCan priorities, roles and responsibilities? With the needs of the forest sector?

Findings: Relevance

Summary:

There is a continued need for the Expanding Market Opportunities program. As the only industry-specific, pan-Canadian program targeting expanding market opportunities for Canadian wood products, this program gives industry the support it needs to create a brand for Canadian forest products and remain competitive in the global market.

The program is well aligned with federal government and NRCan roles, responsibilities and priorities. There is a national interest in the forest sector given its importance to Canada’s economy. The Government of Canada’s commitment to increase exports to overseas markets has grown over the period of evaluation. The program also responds to new commitments under the Pan-Canadian Framework on Clean Growth and Climate Change and to the growth of the bioeconomy.

The EMO program is also aligned with the needs of the forest sector, particularly primary manufacturing. However, specific needs differ among various segments of the forest industry and regions of Canada. Some stakeholders perceive the program to be less well-aligned to the needs of the secondary manufacturing and emerging bioproducts sectors. The nascent bioproducts sector is not yet structured in a way that facilitates its engagement with the EMO program. There are also geographic and structural support barriers to enhanced participation by the forest industry in eastern Canada. While the EMO program has recently introduced new focus areas under its Offshore Markets Component to address some of these concerns, it is still too soon to know their results.

With respect to program relevance, the evaluation recommends:

RECOMMENDATION 1: The Canadian Forest Service should work with partners to address gaps in market research identified by the evaluation and program stakeholders, including developing forward insights into market opportunities for new bioproducts.

MANAGEMENT RESPONSE: Agreed. The Canadian Forest Service will consult with partners to identify and address gaps in the program’s current suite of market studies and strategies, including the market development needs of the emerging bioproducts sector. Due date: March 2023.

There is a continued need for the Expanding Market Opportunities program.

The Expanding Market Opportunities program is designed to ensure a competitive forest sector. It gives Canadian industry the tools it needs to create a national brand for Canadian forest products and remain competitive in the global market. This export-driven sector is highly dependent on trade, particularly with the United States. The EMO program’s support for market diversification responds to a need to reduce the sector’s reliance on this singular export market. Diversification into new export markets provides a buffer against cyclical swings and price volatility. By increasing its potential uses, diversification into new international and domestic market segments also drives an increased demand for wood.

The EMO program is the only industry-specific, pan-Canadian program targeting expanding market opportunities for Canadian forest products. External stakeholders emphasized that without this federal support, work undertaken by industry partners in this area would not take place or would be done at a significantly diminished capacity.

The Expanding Market Opportunities Program is aligned with federal government and NRCan priorities and responsibilities.

The mandate letter of the Minister of Natural Resources (2018) emphasizes that it is a core responsibility of the federal government to help get our natural resources to market. Stakeholders emphasized the importance of federal coordination in this area, ensuring a consistent message to overseas markets of Canada’s wood products “brand” and making it easier for international customers to view Canada as a unified market. This branding is designed to amplify the impact of the program’s international marketing activities.

NRCan’s specific role in the program is supported by the Department of Natural Resources Act (1994), under which the Minister of Natural Resources shall, “participate in the enhancement and promotion of market access for Canada’s natural resources products”. The last evaluation (2016) found that the Canadian Forest Service was well suited to fund and support market access and development activities given its longstanding experience with and knowledge of the forest sector.

The Government of Canada’s commitment to grow new markets and increase exports has grown over the period of evaluation, particularly in response to opportunities presented by new trade agreements secured by Canada in the past three years. The Minister of Natural Resources’ mandate letter (2018) now includes a priority to “identify opportunities to support workers and businesses in the natural resource sectors that are seeking to export their goods to global markets”. The Fall Economic Statement 2018 announced the Government's intention to significantly bolster export opportunities for Canadian businesses and diversify Canada's overseas trade. In response to a Report of the Standing Committee on Natural Resources (May 2018), the Government of Canada committed to continue to provide targeted investments in the forest sector that create new market opportunities both within and beyond Canada’s borders.

There is a national interest in the forest sector given its importance to Canada’s economy.

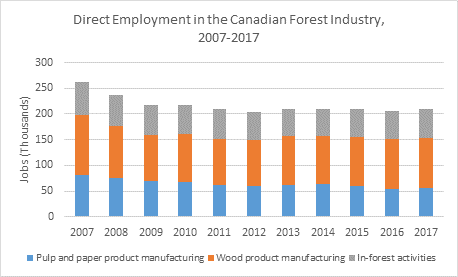

Communities across Canada rely on the forest sector for employment and prosperity. Data in the State of Canada’s Forests (2018) indicates that while the forest industry represents a smaller percentage of Canada’s economy than other resource sectors, it creates more jobs and contributes more to the balance of trade for every dollar of value added than do other major resource sectors. It also has a broader social impact than other major resource sectors, providing employment opportunities across Canada.

Forestry’s contribution is particularly important in many rural and Indigenous communities, where forest-related work is often the main source of income. By helping to ensure a competitive forest sector, the Expanding Market Opportunities program aligns with the Minister of Natural Resources’ mandate commitments to support employment for the middle class by stimulating clean and innovative economic growth and supporting stronger and more resilient rural and Indigenous communities.

Source: State of Canada’s Forests Report, 2018.

Text version

Bar graph showing the trend in the Canadian forest industry's GDP (billions of dollars), 2007 to 2017.

| Year | Pulp and paper product manufacturing | Wood product manufacturing | In-forest activities |

|---|---|---|---|

| 2007 | 82,185 | 115,380 | 64,660 |

| 2008 | 74,870 | 102,080 | 60,540 |

| 2009 | 68,810 | 90,500 | 58,210 |

| 2010 | 67,040 | 93,915 | 56,275 |

| 2011 | 62,490 | 88,680 | 58,425 |

| 2012 | 60,240 | 89,840 | 53,910 |

| 2013 | 62,585 | 93,845 | 53,210 |

| 2014 | 63,895 | 93,405 | 52,675 |

| 2015 | 60,350 | 94,990 | 53,630 |

| 2016 | 54,600 | 97,180 | 53,880 |

| 2017 | 55,590 | 98,570 | 55,780 |

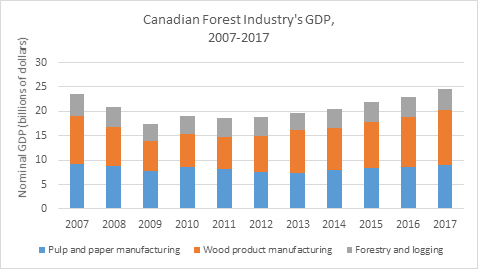

Source: State of Canada’s Forests Report, 2018.

Source: State of Canada’s Forests Report, 2018.

Text version

Bar graph showing the trend in the Canadian forest industry's GDP (billions of dollars), 2007 to 2017.

| Year | Pulp and paper manufacturing | Wood product manufacturing | Forestry and logging |

|---|---|---|---|

| 2007 | 9.3 | 9.7 | 4.46 |

| 2008 | 8.83 | 7.98 | 4.1 |

| 2009 | 7.71 | 6.11 | 3.5 |

| 2010 | 8.58 | 6.81 | 3.64 |

| 2011 | 8.18 | 6.53 | 3.85 |

| 2012 | 7.47 | 7.4 | 3.94 |

| 2013 | 7.42 | 8.79 | 3.39 |

| 2014 | 7.93 | 8.72 | 3.73 |

| 2015 | 8.47 | 9.41 | 4.01 |

| 2016 | 8.53 | 10.25 | 4.12 |

| 2017 | 8.9 | 11.4 | 4.32 |

Source: State of Canada’s Forests Report, 2018.

Increased use of wood in construction supports Canada’s climate commitments and growth of the bioeconomy.

The Pan-Canadian Framework on Clean Growth and Climate Change (2016) outlines new actions for reducing emissions and increasing carbon sequestration via the forest, with specific measures for increasing the use of wood in construction. Research suggests that wood-based materials use less energy and emit fewer greenhouse gases (GHG) and pollutants over their life cycle than traditional construction materials. Consequently, use of wood can help store carbon and reduce the carbon footprint of most buildings. The Brock Commons Tallwood House demonstration project supported by the Expanding Market Opportunities program was recognized at the most recent United Nations’ Climate Change Conference (2018) as an example of international leadership in this area.

Carbon BENEFITS: Brock Commons Tallwood building

Estimates by the Canadian Wood Council, 2018

Volume of wood products used: 2,233 m3

Carbon stored in wood: 1,753 tonnes of CO2 equivalent

Avoided greenhouse gas emissions: 679 tonnes of CO2 equivalent

Climate change is also contributing to a declining fibre supply by increasing natural disturbances, like forest fires and pest infestations. Coupled with the advent of new technology, this places pressure on the forest industry to modernize and diversify products by creating higher value products with lower volumes of inputs. The Forest Bioeconomy Framework for Canada (2017) identifies the unique combination of biomass availability and technical capacity within Canada as an unprecedented opportunity to transition towards a low-carbon, sustainable economy supplied with bio-based solutions. The Standing Committee on Natural Resources (2018) found that the biggest potential for market growth in North America’s value-added sector to be mass timber construction in public, commercial, and high-rise buildings. The federal government thus plays an important and appropriate role in supporting market development activities that drive innovation and transformation in this area.

What is the Bioeconomy?

The bioeconomy refers to the economic activity generated by converting sustainably managed renewable forest-based resources, primarily woody biomass and non-timber forest products, into value-added products and services using novel and repurposed processes. This definition distinguishes between the economic activity generated from producing traditional forest products (e.g., pulp, paper, lumber) and new, advanced bioproducts.

Source: A Forest Bioeconomy Framework for Canada (2017)

The EMO program is aligned with and responsive to the needs of the forest sector.

The EMO program has identified and developed its market strategies and priority markets in collaboration with industry; stakeholders continue to perceive these as appropriate. Given the program’s cost-share requirements (with industry expected to contribute up to 33% of total project cost), continued program uptake by industry is also indicative of its alignment with their needs.

However, specific needs differ among various segments of the forest industry and regions of Canada. The primary manufacturing sector prioritizes advancing opportunities for commodity lumber. The EMO program’s support for wood used in construction, including engineered wood products and innovative new building systems, is well aligned with the current and future needs of this sector. Some stakeholders perceive the program to be less well-aligned to the needs of the secondary manufacturing sector.

Secondary or value-added manufacturers require different export strategies than producers of commodity lumber. This sector consists of mostly family-owned, small and medium enterprises (SMEs). These companies tend to offer a broad diversity of often unique products. As a result, unlike commodity lumber, they tend to differentiate themselves based on the perceived quality of their products, rather than price. The diversity of the sector also means that many of these companies are not necessarily members of or represented by a single industry association. Given that the EMO program is designed to support industry associations, it is thus more challenging to connect with this segment of the wood industry.

The previous two evaluations (2011 and 2016) also found that many of the EMO program’s activities could be better aligned with the needs of secondary manufacturers. For example, value-added companies with diverse, niche products may derive less benefit from tradeshow participation and perceive themselves to be less well represented by the EMO program’s focus area for in-market infrastructure than commodity lumber producers. This sector continues to consider the United States to be its best market opportunity for growth, recognised by many SMEs as a relatively easy entry point to gain experience with exporting, which they can then broaden into other offshore markets.

In response to a recommendation from the last evaluation (2016), the EMO program reviewed options to improve its alignment with and enhance support to the value-added wood products sector. The EMO program has since modified its Terms and Conditions to increase this sector’s engagement. In 2018-19, the CFS added a new focus area for ‘Export-readiness for Secondary Manufacturers’, to support the sector in acquiring the market awareness and the knowledge and skills required for export development for all international markets. In 2019-20, it created an additional new focus area for ‘Secondary Manufacturing - Promotion Activities’ specifically designed to support the promotion and marketing of the sector’s products within the United States. In 2017, the EMO program set a target to have at least three industry recipients representing value-added wood products manufacturers be actively engaged in undertaking market development activities in the US by March 2020.

Text version

Infographic showing that the combination of funding activities for export readiness for secondary manufacturers (2018-19) with activities for the promotion of secondary manufacturing in the US (2019-20) is intended to result in enhanced support to the value-added sector.

Stakeholders view the latter modification in particular as a very positive change for the EMO program. Given that the purpose of the offshore component is to diversify exports away from the US market, it represents a substantial shift in program design to align to the needs of this sector. However, it is still too soon to know the results of these two new focus areas. During the period of evaluation, only one applicant submitted a request for funding under the ‘Export Readiness’ focus area. While outside the temporal scope of the evaluation, a small number of additional requests were made in 2019-20. This should not be interpreted as lack of interest; relevant industry associations require time to consult with their members on the nature of related proposals. In addition, stakeholders noted the new focus areas do not include support for market research in the United States and perceived this gap to be a potential impediment to timely program uptake.

The emerging bioproducts sector will require additional support for market development.

Market access and product promotion are also important components of the innovation continuum to facilitate increased demand for bioproducts. Recognizing the growing importance of the bioeconomy, the EMO program has also recently updated its guidebook for applicants to explicitly include “new bioproducts or next-generation wood products” within the scope of the program’s Offshore Market component (previously implicit).

What are Bioproducts?

Bioproducts are products produced from biomass (biological material). Some examples include fuels, industrial chemicals, pharmaceuticals, textiles and advanced building materials.

Since 2015-16, at least one bioproduct has experienced notable export growth with support of the EMO program (see text box on wood pellets). However, similar to secondary manufacturing, the bioproducts sector as whole is not yet structured in a way that facilitates its engagement with the EMO program – bioproducts are often unique and their producers not members of forest industry associations. While the Canadian market may be an easier entry point for new bioproducts, only products used in construction can be supported by the program’s domestic component under the current Terms and Conditions. More information about the global market for products in this sector is also needed, as it is still unclear which products are mostly likely to be successful.

NRCan’s Evaluation of Forest Sector Innovation Programs (2019) provides more information on needs of the forest bioproducts sector and the performance the CFS’ suite of innovation programs designed to support this sector’s transition to the bioeconomy.

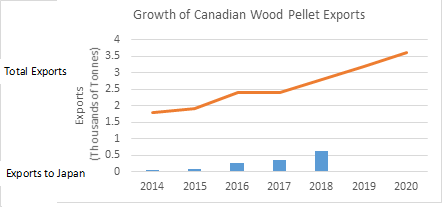

Growth of the Export Market for Canadian Wood Pellets

Wood pellets are a renewable biofuel made from compressed wood fibre. The raw materials for wood pellets are primarily residual by-products of Canada’s lumber industry. Producers of this bioproduct are represented by the Wood Pellets Association of Canada.

As of 2019, there were 40 pellet plants in Canada with an annual capacity of 4 million tonnes. In 2017, this represented 9% of world wood pellet production. Canada exports an estimated 90% of its wood pellet production.

Text version

Graph showing the growth of Canadian wood pellet exports (thousands of tonnes), 2014 to 2020.

| Year | Total Exports | Japan |

|---|---|---|

| 2014 | 1800 | 62 |

| 2015 | 1900 | 80 |

| 2016 | 2400 | 272 |

| 2017 | 2400 | 360 |

| 2018 | 2800 | 630 |

| 2019 (forecast) | 3200 | n/a |

| 2020 (forecast) | 3600 | n/a |

Source: Statistics Canada and Canadian Wood Pellet Association

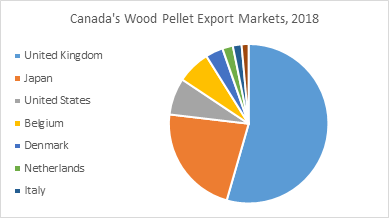

Text version

Pie chart depicting Canada’s wood pellet export markets (thousands of tonnes), 2018.

| Country | Exports |

|---|---|

| United Kingdom | 1530 |

| Japan | 630 |

| United States | 210 |

| Belgium | 190 |

| Denmark | 100 |

| Netherlands | 60 |

| Italy | 50 |

| South Korea | 40 |

There are geographic and structural support barriers to enhanced participation by the forest industry in eastern Canada.

Forest operations take place in all regions of Canada except the Far North. Of the total forest industry jobs in Canada, 52% are in Ontario and Quebec, 39% are in western Canada (with the vast majority in British Columbia), and 9% are in Atlantic Canada.

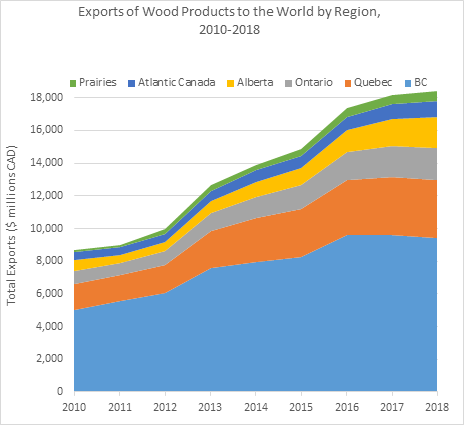

We found that the EMO program is well aligned to the needs of the forest industry in western Canada, as demonstrated by the program’s long-standing partnership and harmonization with the Government of British Columbia’s Forestry Innovation Investment (BC FII). While forest producers in eastern Canada perceive the expected results of the EMO program to be aligned with their needs, they also face a geographic barrier to cost-effectively accessing the Asian markets heavily invested in by the program. Stakeholders in these provinces are also more challenged to leverage funds for proposed projects as, except in Quebec, there are few provincial funding programs with a similar design and delivery focused on expanding market opportunities for the forest industry. Regardless, we found indications of progress in leveling the playing field. From 2010-2018, all provinces except those in Atlantic Canada have increased their exports of wood products at a rate exceeding that of British Columbia.

Source: Statistics Canada via Global Trade Atlas (April 1, 2019)

Text version

Graph of trend in exports of Canada’s wood products to the world, by region of Canada (in millions of dollars), 2010 to 2018.

| Year | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 |

|---|---|---|---|---|---|---|---|---|---|

| BC | 4,994 | 5,591 | 6,053 | 7,613 | 7,982 | 8,255 | 9,601 | 9,577 | 9,429 |

| Quebec | 1,608 | 1,557 | 1,711 | 2,225 | 2,686 | 2,913 | 3,372 | 3,582 | 3,537 |

| Ontario | 801 | 745 | 855 | 1,117 | 1,233 | 1,464 | 1,700 | 1,865 | 1,957 |

| Alberta | 644 | 499 | 545 | 712 | 953 | 1,083 | 1,338 | 1,694 | 1,914 |

| Atlantic Canada | 505 | 471 | 502 | 610 | 695 | 734 | 824 | 891 | 956 |

| Prairies | 140 | 157 | 284 | 372 | 357 | 392 | 532 | 563 | 612 |

What We Found

Effectiveness

Were recommendations from past audits, evaluations (and other reviews) effectively implemented? Are resulting management actions showing positive results?

Has the program been responsive to internal and external factors impacting the program’s ability to achieve its intended outcomes and operate with efficiency? How and to what extent?

To what extent do activities of the program continue to result in expected outcomes?

FINDINGS: Effectiveness

Summary:

We found that the Expanding Market Opportunities program has been responsive to factors affecting its ability to achieve its intended outcomes and operate with efficiency, including global competition, market volatility, and forest sector innovations. The program continues to demonstrate a strategic approach to identifying and pursuing opportunities for market diversification. Moving forward, it will be important to ensure that these international activities remain aligned with NRCan’s broader strategic framework for international activities and new International Departmental Plan.

Market diversification requires years of sustained effort. We found evidence of continued progress towards achievement of the program’s intended outcomes for its Offshore Markets component. Overall, the volume and value of wood products sales in targeted international markets continues to increase. While numerous external factors make it a challenge to attribute these results directly to the EMO program, there is anecdotal evidence to suggest that the program’s market development and market access activities have contributed towards the results achieved. Forest product stakeholders continue to be engaged in international market development activities. The EMO program is effectively addressing regulatory, environmental and technical barriers to international market access. There has also been increased awareness of wood products and construction technologies among end users.

Domestically, stakeholders perceive the EMO program to be a “game-changer” for increasing wood use in North American non-residential and mid-rise construction. The program’s support for technical research and testing has contributed to amendments to building codes, creating an enabling environment for building with wood and contributing to the growing market for new building systems. Uptake in wood construction has also been effectively supported by information, education and capacity building. Corporate targets to increase the dollar value of wood products used in domestic non-residential construction projects were exceeded. Further efforts towards broader domestic adoption and commercialization of wood in construction could be facilitated by increasing the program’s reach to new target audiences.

Program activities also continue to result in achievement of expected outcomes for Canada’s environmental reputation. Targeted international markets consider Canadian forest products to be an environmentally responsible choice. This strong brand gives Canada a competitive advantage. Current success is such that some stakeholders perceive Canada’s reputation for sustainable forest management is now less well regarded at home than it is internationally. Better communication within Canada of the forest industry’s environmental performance and wood’s environmental benefits could support domestic marketing of wood as a preferred option for sustainable construction.

With respect to program effectiveness, the evaluation recommends:

RECOMMENDATION 2: The Canadian Forest Service should review its pilot of in-market infrastructure in the Middle East, ensuring that it is aligned with NRCan’s broader international strategy. CFS should also share its lessons learned from this review so as to inform NRCan’s implementation of similar positions in other sectors.

Management Response: Agreed. In April 2019 the Canadian Forest Service contracted with a consulting firm specializing in evaluation and performance management to perform an impact assessment of the pilot in-market infrastructure in the Middle East. Lessons learned will inform the future of the pilot and be shared within the department at the Directors General International Affairs Committee. Due date: March 2020.

RECOMMENDATION 3: The Canadian Forest Service should work with domestic partners to extend outreach to new target audiences in the delivery of the North American Markets component, including considerations for more innovative use of online media.

Management Response: Agreed. The Canadian Forest Service will work with domestic partners to increase engagement with different target groups in the delivery of the North American Markets component. This includes launching new education programs with insurers, information campaigns on the implications of the 2020 National Building Code, and investing in enhancements to the Think Wood online communications platform as well as those of other industry stakeholders. Due date: May 2020.

RECOMMENDATION 4: The Canadian Forest Service should work with partners to increase communication of the forest industry’s environmental performance within Canada and the domestic marketing of wood as a preferred option for sustainable construction.

Management Response: Agreed. The Canadian Forest Service will work with partners to improve communication of the forest industry’s environmental performance within Canada and the domestic marketing of wood as a preferred option for sustainable construction. The program will partner with industry on a National Sustainability Coordinator position at the Canadian Wood Council that will increase awareness and reduce/remove barriers and misinformation related to wood use in sustainable construction, and to position wood as the building material of choice, based on science. Due date: May 2020.

The program has been responsive to factors affecting its ability to achieve its intended outcomes and operate with efficiency.

This evaluation examined the changes in context impacting on the program since the last evaluation. We found that the EMO program is well designed to respond to increasing global competition and trade uncertainty. Global competition influences competitiveness and reinforces the need for diversification. While numerous external factors (e.g., global demand and supply dynamics) make it a challenge to attribute results in market diversification directly to the EMO program, there is evidence to suggest that the EMO program’s market development and market access activities have contributed towards the results achieved.

Stakeholders generally agreed with Canada’s approach to market diversification, i.e., working to build the relationships required to grow a small number of target markets rather than spread resources thinly over numerous markets.

Country-based market strategies for key markets (i.e. China, Japan, South Korea, and Europe) guide the direction of the Offshore Markets component. While at a high level all markets share the same business goal (i.e., to maintain or increase the volume and value of Canadian wood product exports), priority market segments vary by market. Market strategies were recently updated (2017) in consultation with industry and provincial funding partners to account for the impact that in-market trends and changing demographics can have on demand for wood products.

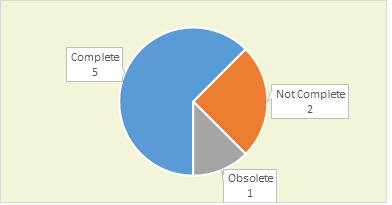

Status of Past Management Actions

This evaluation examined the extent to which management actions in response to previous recommendations (2016) had been effectively implemented, and whether the actions taken have had a positive impact on the program’s performance.

Results are summarized in Appendix 3. These management actions and their impacts are also highlighted where relevant in this evaluation report. Actions that are not yet complete have had their targeted completion date revised to March 2020.

Text version

Pie chart showing 5 complete management actions from the previous evaluation’s recommendations, 2 incomplete actions, and 1 obsolete action.

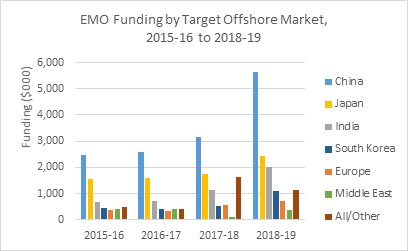

While there has been no significant increase in the number of targeted export markets since 2015-16, exploratory work is now underway in India, Vietnam, the Middle East, and Caribbean.

Text version

Bar chart comparing the EMO program’s funding by target offshore market (thousands of dollars), 2015-16 to 2018-19.

| Market | 2015-16 | 2016-17 | 2017-18 | 2018-19 |

|---|---|---|---|---|

| China | 2,476,503 | 2,583,962 | 3,155,835 | 5,619,440 |

| Europe | 382,900 | 358,637 | 563,007 | 712,970 |

| India | 684,913 | 713,128 | 1,138,475 | 2,009,302 |

| Japan | 1,551,806 | 1,614,524 | 1,755,461 | 2,444,390 |

| Middle East | 511,501 | 522,372 | 114,921 | 403,230 |

| South Korea | 465,703 | 420,240 | 536,514 | 1,116,490 |

| All/Other | 509,116 | 421,636 | 1,624,132 | 1,145,975 |

Source: EMO Program Data

Given their geographic proximity, the Middle East and Caribbean markets are expected to better address market opportunities for forest products from eastern Canada. However, industry stakeholders had mixed views of the prospective Middle Eastern market. Intended as a pilot, this is the only market for which the EMO program funds in-market staff through transfers to Global Affairs Canada (i.e., a trade commissioner in the Canadian Embassy in Abu Dhabi).Footnote 1 Most respondents agreed it makes sense for Canada to develop a presence in this market, yet many still view it as a niche market where current potential is relatively limited. The view of this market was somewhat more positive among those in the value-added sector.

Other sectors of NRCan also engage in activities abroad, in locations where market access, commercial opportunities, and collaboration in science and technology offer the most potential for Canada. A recent internal Audit of the Management of International Activities (2019) found that NRCan could improve its strategic planning in this area. In response, the department has committed to establishing a strategic framework to identify its key international priorities and objectives, including an annual International Departmental Plan. Moving forward, it will be important to ensure that the EMO program’s international activities are aligned with this approach.

To address resource capacity issues and support cross-sectoral market diversification efforts, NRCan is also now developing a similar initiative to pilot a limited number of dedicated in-market positions with horizontal natural resources expertise. Lessons learned from a review of the EMO program’s pilot initiative in the Middle East could help inform the implementation of these positions.

Trade uncertainty and market access issues to new and existing markets are challenges for export growth.

While the U.S. remains a key market for Canadian forest products, the softwood lumber dispute is an on-going challenge for the industry. The volatility of this trade dispute and Canada’s relationship with the U.S. demonstrate a continued need to diversify. The EMO program’s long-term vision is thus critical to ensure that Canada remains competitive. However, Canada has also introduced additional measures in response to this dispute. In June 2017, the EMO program received $45M over three years to support efforts under the Softwood Lumber Action Plan (SLAP). This injection extended the program to March 2020. With this increased funding, the EMO program also introduced short-term flexibilities in cost-share provisions that enable NRCan to contribute up to 100% of project costs for focus areas related to market access under the program’s international component. The program has also increased its efforts to support large-scale demonstration projects in key markets where such projects could help accelerate market development by showcasing the use of wood in construction.

The Canadian Forest Service is also working with other government departments to ensure forest sector needs are reflected in new trade agreements. New trade agreements negotiated over the period of evaluation – e.g., the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP), Canada-European Union Comprehensive Economic and Trade Agreement (CETA), and Canada United States Mexico Agreement (CUSMA) – present opportunities for expanded trade. With support from the EMO program, the use of wood and wood products that are the result of sustainable forestry practices is now also being encouraged in other partnership agreements, such as the Canada-China Joint Leaders’ Statement on Climate Change and Clean Growth (2017).

Regardless, increasing global competition creates a risk that competitors will take advantage of Canada’s market development efforts. The EMO program is responding to this risk by driving an increased demand for wood, while also building a strong brand and positive reputation for Canadian wood. By ensuring that codes and standards in offshore markets are consistent with Canadian practices, promoting the attributes of Canadian species and Canada’s environmental reputation, and developing strong relationships, the EMO program works towards creating a competitive advantage for Canada.

Most emerging trends are on the EMO program’s radar, but more emphasis on new technology and bioproducts may be needed.

New technology is changing the demand for traditional forest products while creating innovative new products. For example, Cross-Laminated Timber (CLT) is becoming increasingly popular among architects, builders, and engineers for being an environmentally friendly material suitable for multi-storey buildings. While in wide use in Europe since the 2000s, the demand for and manufacturing of this product is just starting to grow in North America. The EMO program has supported technology testing, technical transfer, training, commercial uptake and regulatory acceptance in response to the growing demand for this and other innovative wood products and construction applications.

However, limitations in Canadian manufacturing supply for advanced wood products is an emerging issue for market growth. Canada currently has very few manufacturers of certain wood products required for more advanced wood construction. For example, there are only a few small production facilities for CLT in North America, and Atlantic Canada currently does not have any manufacturers of mass timber. As a result, parts of Canada lack the capacity to support a sudden increase to high levels of demand. Clear demand signals, including but not limited to demonstrations of tall wood buildings, could serve as a catalyst for industry to initiate or increase production in this area. To that end, some stakeholders suggested that increasing the number of advanced wood structures in rural areas (closer to where manufacturing takes place) would provide opportunities for producers to directly observe this potential.

In 2018, the Canadian Forest Service launched the Green Construction through Wood (GCWood) program to amplify domestic support and showcase opportunities for innovative wood construction. While shifting related activities away from the EMO program, GCWood provides more dedicated funding for domestic wood demonstration projects. It also supports revisions to the building code and advancing wood education at Canadian engineering and architectural schools. All stakeholders viewed this shift as a positive development.

Program activities continue to result in expected outcomes for international markets.

The Offshore Markets component seeks to expand the export opportunities of Canadian wood producers in traditional and emerging markets by providing forest industry associations and other stakeholders with the capacity to act on those opportunities through funding for international export development activities. Its targeted outcomes focus on the engagement of stakeholders to explore and pursue opportunities in new markets, addressing barriers to market access, and ultimately, the diversification of export markets and market segments for Canada’s forest industry. The following summarizes the evaluation’s findings on progress against these outcomes.

Forest product stakeholders continue to be engaged in international market development activities.

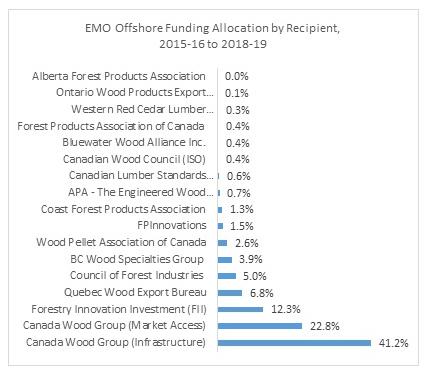

Over the period of evaluation, the number of industry associations participating in the Offshore Markets component of the program remained relatively stable, with an average of 10 organizations participating each year. Most major forest companies involved in primary manufacturing and numerous secondary manufacturers are represented by one or more participating associations. Wherever possible, the program requires market access activities to be coordinated and delivered through the Canada Wood Group, to deliver benefits to the Canadian forest industry as a whole.

Text version

Bar chart comparing the EMO program’s total offshore funding allocation by recipient, 2015-16 to 2018-19.

| Organization | Percent of Total Funding |

|---|---|

| Alberta Forest Products Association | 0.0% |

| Ontario Wood Products Export Association | 0.1% |

| Western Red Cedar Lumber Association | 0.3% |

| Forest Products Association of Canada | 0.4% |

| Bluewater Wood Alliance Inc. | 0.4% |

| Canadian Wood Council (ISO) | 0.4% |

| Canadian Lumber Standards Accreditation Board | 0.6% |

| APA - The Engineered Wood Association | 0.7% |

| Coast Forest Products Association | 1.3% |

| FPInnovations | 1.5% |

| Wood Pellets Association of Canada | 2.6% |

| BC Wood Specialties Group | 3.9% |

| Council of Forest Industries | 5.0% |

| Quebec Wood Export Bureau | 6.8% |

| Forestry Innovation Investment (FII) | 12.3% |

| Canada Wood Group (Market Access) | 22.8% |

| Canada Wood Group (Infrastructure) | 41.2% |

Over the period of the evaluation, the EMO program has supported the Canada Wood Group to maintain in-market infrastructure (i.e., staff and offices) in China, South Korea, Japan, and the UK (for the EU market). Since 2016-17, it has also supported the Canada Wood Group to open two new offices in India. These are satellite offices to an office in Mumbai operated by BC FII; an office that the EMO program has supported since 2012. By facilitating the building of in-market relationships and networks, most stakeholders view this on-the-ground capacity as critical to amplifying the impact and reach of offshore market development activities. It also allows the industry to gain timely market information that helps capture business opportunities and respond to market access issues, giving Canadian companies a competitive advantage against competitors that do not have a similar in-market presence.

Having the information required to identify market changes and pursue market opportunities has been instrumental in continued stakeholder engagement. Market research on new and/or existing markets supported by the EMO program has enabled forest companies to better align operations with customer demands. Funding provided by the EMO program for market research has also supported the information needs of specific industry segments where target markets differ from those for commodity lumber, such as wood pellets, and of regions in Canada with less ready access to the Asian market. However, a few stakeholders still identified more work required in this area, such as detailed market studies of opportunities in new markets and reviews of the advantages opened by new international trade agreements (e.g., the Comprehensive Economic Trade Agreement with Europe). In addition, several stakeholders also viewed developing forward insights into market opportunities for new bioproducts as an area that will require more focus in the near future.

The EMO program is effectively addressing regulatory, environmental and technical barriers to international market access.

Addressing barriers to market access is an important foundation for market diversification. The trend in access to export markets over the period of evaluation differed across markets. As previously noted, access to the US market has declined as a result of the softwood lumber dispute. However, access to other markets has improved both as a result of the work of the EMO program and new international trade agreements. There is a need for continuous work in this area as countries introduce new or amended regulatory or technical requirements. However, there is evidence of progress:

- Regulatory agencies are being provided with the information they need to determine product performance and environmental credentials. Support from the EMO program has been instrumental for completing and promoting the results of technical research and product testing (e.g., seismic stability, fire resistance) to respond to changing performance demands and updates to national building codes. This includes some multi-year research, such as international field tests to show the resistance of treated Canadian wood to decay and pests. Besides being an opportunity to work through technical issues, offshore demonstration projects supported by the EMO program have become focal points to showcase what is possible when building with wood, to facilitate the interest of architects and engineers, and enable discussions of in-market business cases (e.g., cost savings).

- There has been increased regulatory acceptance and recognition of Canadian wood products and building systems in foreign codes, standards and policies. Canada’s ability to draw on technical expertise to demonstrate fire, seismic and other structural characteristics of Canadian products – along with the trust built up among key actors over the years – has been critical in influencing the development of codes, standards and policies in offshore markets. For example, in 2003, no policies or codes for wood frame construction existed in China. From 2003 to 2017, work of the Canada Wood Group drove the development of over 175 new codes, standards and related government policies. The accumulation of these achievements means that China is now a viable market for wood construction. This would not have been possible for industry acting alone; besides financial support, the EMO program’s public-private model gave the Canada Wood Group access to government building code committees.

- There has been increased awareness of wood products and construction technologies among end users. Code changes are necessary but not sufficient to increase the use of wood; building codes enable wood construction but do not provide technical guidance on how to build with wood. There is a risk that public perceptions of wood construction will be negatively impacted if structures are not properly executed (resulting in fire or structural deficiencies). However, EMO program staff and stakeholders perceive this risk to be low provided there is effective technology transfer and training. From 2015-16 to 2017-18, on average the EMO program supported close to 80 offshore training sessions per year, reaching thousands of builders, designers, inspectors, instructors and university students. The intended impact goes beyond transferring knowledge; the participants also develop a familiarity and preference for Canadian wood products. A recent (2017) survey of industry representatives supported in part by the EMO program shows that Canada’s technical knowledge is highly regarded in Japan, South Korea and China, with Canada ranking first or second among its competitors as a leader in wood construction technology. Canada’s growing domestic experience in building with wood and tall wood buildings likely assists with this reputation, resulting in increased demand for its products and services.

While the EMO program clearly contributes to market access, not all progress in this area can be attributed to the program. The CFS also works outside of the EMO program in partnership with other federal government departments, provincial governments and the forest industry to help address forestry-related trade irritants, market access and market acceptance issues.

Long-term trends in key target markets indicate progress towards diversification of markets and market segments.

Over the period of evaluation, the EMO program has measured its progress towards the diversification of markets for Canadian forest products in two ways:

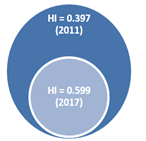

Measuring Diversity with the Herfindahl Index

The Herfindahl Index (HI) is an inverse measure of Canadian export diversification (i.e., a concentration ratio). Its values range from ‘0’ and ‘1’, with values close to ‘0’ representing greater diversification of exports. This index shows the market for Canadian forest products becoming less diverse since 2011.

Text version

Infographic showing the Herfindahl Index at 0.397 in 2011 and 0.599 in 2017, indicating decreasing diversity of the market for Canadian forest products since 2011.

- Herfindahl Index – The EMO program has used this index to measure Canada’s success in diversifying its wood product exports away from the US and towards offshore markets over time.Footnote 2 Corporate reporting shows that the program did not meet its target for this Index during the period of evaluation. Rather, since 2011, the trend in this index shows the market for Canadian forest products becoming increasingly concentrated. A key factor contributing to this trend is the strong demand for wood products by the United States, which continues to take a larger share of Canadian exports relative to offshore destinations. Recent changes in program design, particularly the new focus area for ‘Secondary Manufacturing - Promotion Activities’ designed to support the marketing of the sector’s products within the United States, is not likely to assist in reversing this trend.

- Increased value of wood products sales in targeted offshore markets – We found that the EMO program met its corporate target to increase the dollar value of wood product sales in existing offshore markets (China, Korea, Japan and Europe) by 10% over the 2011 values by March 2017. In 2017-18, total wood sales to these markets were estimated at $3.6 billion. While the EMO program did not meet a parallel target for new emerging markets (e.g., India and Middle East), detailed results show high levels of year-to-year fluctuations and country-to-country variability. These fluctuations are not unexpected with immature emerging markets.

Target Market ∆ 2011 to 2017 Result Existing Markets ↑16.1%

($3.1B to $3.6B)Target exceeded. Emerging Markets ↓35%

($99.3M to $64.5M)Target not met.

The program has since targeted an additional 5% increase in the value of offshore wood product exports for both existing markets and high-potential emerging markets by 2023. Data are not yet available to inform progress against these targets.

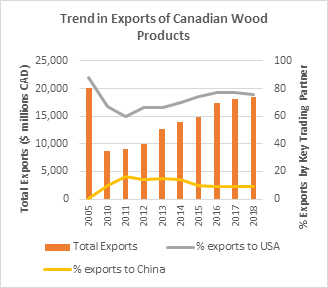

However, consideration of these short-term results is insufficient to effectively judge the program’s performance. Market transformation requires years of sustained effort. The long-term trend shows clear indications of progress in key target markets. Since 2005, the percentage of Canadian wood product exports directed to the United States has decreased from 88% to 76% (2018). Meanwhile, China has grown significantly as a market. Evidence indicates that Canada now dominates market share for wood construction in China, with 90% of modern wood structures using Canadian wood.

Text version

Graph showing the trend in total exports of Canadian wood products (in millions of dollars), and the trend of Canadian wood exports to key trading partners (United States and China) as a percentage of total exports, 2005 to 2018.

| Year | 2005 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 |

|---|---|---|---|---|---|---|---|---|---|---|

| Total Exports (millions of dollars) | 20,148 | 8,692 | 9,021 | 9,951 | 12,649 | 13,906 | 14,841 | 17,367 | 18,173 | 18,406 |

| Percent of exports to USA | 88 | 67 | 60 | 66 | 66 | 70 | 74 | 77 | 77 | 76 |

| Percent of exports to China | 0.5 | 10 | 16 | 14 | 15 | 14 | 10 | 9 | 9 | 9 |

Looking forward, we found that tracking the results of export diversification may become increasingly difficult with the growth of the bioeconomy. New bioproducts use components from a variety of other sectors, which makes standardized classification and categorization increasingly difficult. The lack of coherent data can lead to biased perspectives of forest products, both in underestimating diversification and overestimating the scale or pace of changes.

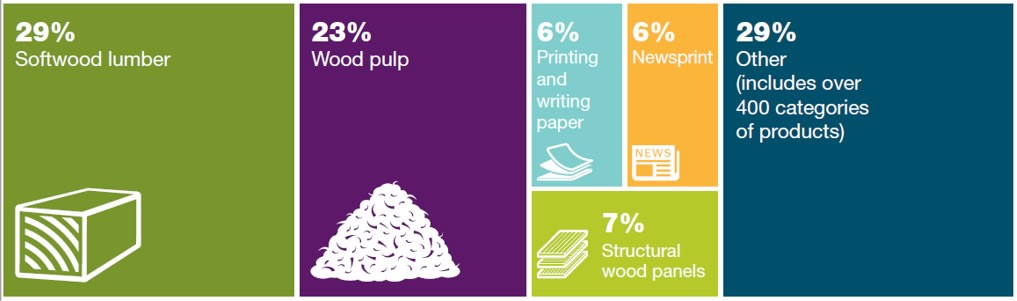

Exports of Canadian Forest Products (2017)

Source: State of Canada’s Forests (2018)

Text version

Infographic showing the breakdown of exports of Canadian forest products in 2017: 29% were softwood lumber, 23% wood pulp, 7% structural wood panels, 6% printing and writing paper, 6% newsprint, and 29% other (includes over 400 categories of products). Source: State of Canada’s Forests (2018).

Program activities continue to result in expected outcomes for domestic markets.

The North American Markets component builds capacity to increase the use of wood in non-residential and mid-rise construction in Canada through funding for the generation and dissemination of knowledge needed by end-users (i.e., architects, specifiers, builders, engineers and designers). Its targeted outcomes include the diversification of market segments for Canada’s forest industry. The following summarizes the evaluation’s findings on progress against these outcomes.

The Canadian Wood Council and WoodWORKS! perceive the EMO program to be a “game-changer” in domestic markets.

Wood WORKS! is a pan-Canadian program run by the Canadian Wood Council. Its mission is to expand market access and increase demand for wood products in the non-residential, mid-rise and tall wood building markets in Canada. It seeks to build proficiency in using wood through training, networking and direct technical support. The organization has five regional offices – British Columbia, Alberta, Ontario, Quebec (where it is called Cecobois), and Atlantic.

The EMO program supports industry representation by domestic technical advisors directly involved in the delivery of WoodWORKS! (i.e., staff, offices and associated expenses). Without the financial support and vision adopted by the EMO program over the last 10 years, related stakeholders posit that Canada “would not see architects, engineers and builders embracing wood to the extent we see today”.

We found that the role of WoodWORKS! has evolved over the past 20 years from a focus on a few small projects to now working to influence entire communities built with wood (including high-rise, commercial and institutional structures). Stakeholders noted an increased interest from forest companies to engage with the program as opportunities for mid-rise and tall wood buildings increase. However, there is still significant room to grow. Stakeholders predict that the more visible these opportunities become, the more engaged industry will be.

Amendments to building codes have created an enabling environment for building with wood.

Similar to market access in the Offshore Markets component, there are two basic elements required to enhance the capacity to use Canadian wood products in non-residential, mid- and high-rise construction: regulatory acceptance and technical knowledge. Within Canada, the base of success for increasing the use of wood in construction is revision of building codes. In 2015, the National Building Code of Canada (NBCC) was revised to increase the height limit of wood buildings from four to six storeys. Each cycle of this code takes five years, and requires extensive research and development (R&D). Over the period of evaluation, R&D activities required to support the building code revisions for wood construction were funded by the EMO program as part of a broader set of NRCan investments, and in conjunction with other funding partners.

The EMO program has also helped advance the adoption of provincial codes and standards related to mid-rise wood frame construction. However, progress within each province has been uneven. The Government of British Columbia amended the BC building code in 2009 to allow mid-rise wood frame construction, ahead of the NBCC 2015. The provinces of Alberta, Saskatchewan, Ontario, Quebec, Nova Scotia and Newfoundland have since also amended their building codes. WoodWORKS! continues to work with other provinces to influence this change.

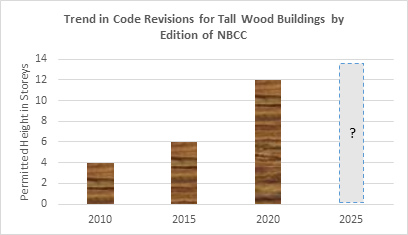

In August 2015, Quebec became the first jurisdiction in North America to officially support the construction of tall mass timber buildings (up to 12 storeys). The foundation for Quebec’s supporting directives and technical guide was a demonstration project realized with support from the EMO program’s Tall Wood Building Demonstration Initiative (TWBDI). From 2013 to 2017, the EMO program managed the TWBDI with the goal of fostering commercial and regulatory uptake of tall wood buildings in Canada. Technical information developed in support of the design and construction of the demonstration buildings has been used to support proposed changes to the 2020 edition of the NBCC, with revisions targeting tall wood buildings up to 12 storeys – well beyond the current limit. Looking forward to 2025, further revisions are proposed to move beyond prescriptive height limits to a performance-based code. These updates aim to level the playing field for wood as a construction material.

Text version

Graph of the trend in height of tall wood buildings (in storeys) permitted in code revisions by edition of the National Building Code of Canada, 2010 to 2025.

| Year | 2010 | 2015 | 2020 | 2025 |

|---|---|---|---|---|

| Permitted Height in Number of Storeys | 4 | 6 | 12 | To be determined |

Tall Wood Building Demonstration Initiative (TWBDI)

The TWBDI provided critical funding for the incremental research and development activities required to design, approve and construct two tall wood building demonstration projects.

Brock Commons Tallwood House (Vancouver)

- TWBDI contribution: $2.33 million.

- At the time of its construction, the tallest contemporary wood building in the world (18 storeys).

- Funds contributed to design, approval, construction, structural and fire testing, and enhancement of construction site safety.

Origine Eco-Condos (Quebec City)

- TWBDI contribution: $1.2 million.

- Tallest all-wood condominium in North America (13 storeys).

- Funds supported design, approval and construction, and critical research on fire resistance, structural and acoustics. The building design was based on EMO-funded tall wood technical guide by FPInnovations.

These demonstration projects showcase the application, feasibility and environmental benefits of innovative wood-based structural solutions. NRCan’s support for domestic demonstration projects continues but was transferred to its new GCWood Program in 2018-19.

Stakeholders noted that the impacts of demonstration projects and other CFS investments in innovation reach beyond Canada to positively influence results in offshore markets. Domestic engagement in the use of wood, particularly as demonstrated by the application of new wood products and innovative building systems, is important to build credibility and encourage uptake in offshore markets.

Uptake in wood construction has been supported by information, education and capacity building.

As previously noted, code changes are necessary but not sufficient to increase the use of wood. Knowledge of working with new structural systems is just starting to emerge, and end-users (architects, engineers, developers, builders, etc.) need technical assistance to understand how to incorporate and optimize wood in design. While the flexibility afforded by wood appeals to architects and designers who can use this material to generate creative aesthetic designs, it is still a challenge to find engineers and builders experienced in working with wood that can easily achieve this vision. Increasing the capacity to work with wood is thus critical to influencing its use in mid- and high-rise and non-residential construction applications. To this end, the EMO program supports WoodWORKS! to develop technical materials and deliver both one-on-one technical support and broader training opportunities (average of 50,000 hours of training attained by end users each year). WoodWORKS! makes related technical materials available in print and on-line via its website. The EMO program is also supporting the BC Forestry Innovation Investment to optimize the Think Wood! communications platform (a US-based repository of information on wood construction) with a focus on incorporating Canadian content. Without these efforts, end-users’ capacity to build with wood would likely be significantly diminished.

In 2017-18, the EMO program supported the Canadian Wood Council to develop an “Advanced Wood Education Roadmap” designed to better integrate wood into the curricula of engineering and architectural colleges and universities. This initiative is intended to address a gap in post-secondary education required to supply Canada’s labour market with well-prepared entrants and create a more diverse supply of domestic expertise. Implementation of the roadmap began in 2018, funded under the new GCWood program. While it is too soon to know the results of this initiative, many stakeholders had a positive view of the Education Roadmap and commented on its importance to supporting the objectives of the North American component of the EMO program.