Audit of Investment Planning and Reporting (AU1701)

Audit Branch

Natural Resources Canada

Presented to the Departmental Audit Committee (DAC)

December 15, 2016

TABLE OF CONTENTS

EXECUTIVE SUMMARY

INTRODUCTION

Departmental investment planning has been defined by the Treasury Board Secretariat (TBS) as the function of allocating and reallocating resources to new and existing assets and acquired services that are essential to program delivery. Deputy Heads are responsible for effective investment planning as a key element in achieving value for money and sound stewardship of public resources.

Investment planning is primarily governed by the TBS Policy Framework for the Management of Assets and Acquired Services, which includes the TBS Policy on Investment Planning – Assets and Acquired Services and the Policy on the Management of Projects, both of which became effective in December 2009. TBS has also developed a Guide to Investment Planning – Assets and Acquired Services to assist departments in implementing these policies. The three types of investments defined under the Policy Framework are:

- Assets – tangible and intangible items of value that have a future life beyond one year;

- Acquired services – services obtained through formal arrangements to support internal or external clients or stakeholders in achieving specific outcomes (e.g., training, call-centre support); and,

- Projects – activities or a series of activities that have a beginning and an end.

The TBS Policy on Investment Planning – Assets and Acquired Services requires that federal departments submit formal five-year investment plans at a minimum of every three years and defines specific requirements for their content as well as the monitoring and reporting requirements of investment planning.

The Department of Natural Resources Canada’s (NRCan’s) Investment Planning Office, within the Corporate Management and Services Sector (CMSS), with input from Sector planning offices has prepared three investment plans under the TBS Policy Framework. The previous investment plan covering the five-year period from 2013-14 to 2017-18 included $1,448 million in planned spending on reportable investments. The current departmental investment plan covers the period from 2016-17 to 2020-21 and includes $237.8 million in planned spending on reportable investments. Most of the decrease is attributed to: investments that were completed, the transfer of responsibilities for Port Granby and Port Hope to Atomic Energy of Canada Limited, and the refining of NRCan’s definition of a reportable investment. In 2015-16 a five year capital asset plan (2016-17 to 2020-21) was also developed to capture the Department’s existing capital assets and highlight future asset needs. NRCan’s Vote 5 capital spending authority for 2016-17 is $53.3 million. The current plan was submitted to TBS for feedback in October 2016.

Text version

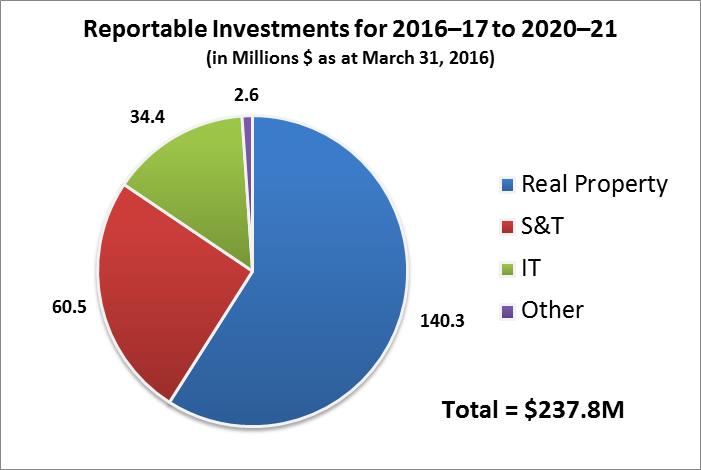

This figure illustrates the distribution by category of the ongoing and future reportable investments included in NRCan’s 2016-17 to 2020-21 investment plan, valued at a total of $237.8 million. The distribution of reportable investments is as follows: $140.3 million for investments in real property, $60.5 million for investments in Science & Technology, $34.4 million for investments in Information Technology, and the remaining $2.6 million for ‘other’ investments that do not fall into any of the other categories.

The objective of this audit was to assess the management control framework and processes in place to support the development of the departmental investment plan.

STRENGTHS

The audit identified that governance structures have been established to support departmental investment planning, and priority determination criteria have been developed to support decision making with respect to internal departmental funding requests. The audit also identified that various efforts have been made to streamline the investment planning process, including leveraging related financial exercises and developing standard tools and templates to support monitoring.

AREAS FOR IMPROVEMENT

The audit identified opportunities to improve the current investment planning monitoring and reporting framework, including communication of roles and responsibilities and guidance to support governance bodies in their decision making. The audit also identified opportunities to align current investment planning processes with other related corporate planning exercises and to better align the presentation of the investment plan with the requirements of applicable Treasury Board Policies.

INTERNAL AUDIT CONCLUSION AND OPINION

In my opinion overall, many efficiencies in the investment planning processes have been gained from the lessons learned through the development of the previous investment plan. The audit identified opportunities to further integrate investment planning with related corporate planning exercises and to improve the alignment of the investment plan with Treasury Board guidance to support an improved monitoring and reporting framework.

STATEMENT OF CONFORMANCE

In my professional judgement as Chief Audit Executive, the audit conforms with the Internal Auditing Standards for the Government of Canada, as supported by the results of the Quality Assurance and Improvement Program.

Christian Asselin, CPA, CA, CMA, CFE

Chief Audit Executive

December 15, 2016

ACKNOWLEDGEMENTS

The audit team would like to thank those individuals who contributed to this project and, particularly employees who provided insights and comments as part of this audit.

INTRODUCTION

Departmental investment planning has been defined by the Treasury Board Secretariat (TBS) as the function of allocating and reallocating resources to new and existing assets and acquired services that are essential to program delivery. Deputy Heads are responsible for effective investment planning as a key element in achieving value for money and sound stewardship of public resources.

Investment planning is primarily governed by the TBS Policy Framework for the Management of Assets and Acquired Services, which includes the TBS Policy on Investment Planning – Assets and Acquired Services and the Policy on the Management of Projects, both of which became effective in December 2009. TBS has also developed a Guide to Investment Planning – Assets and Acquired Services to assist departments in implementing these policies. The three types of investments defined under the Policy Framework are:

- Assets – tangible and intangible items of value that have a future life beyond one year;

- Acquired services – services obtained through formal arrangements to support internal or external clients or stakeholders in achieving specific outcomes (e.g. training, call-centre support); and,

- Projects – activities or a series of activities that have a beginning and an end.

The TBS Policy on Investment Planning – Assets and Acquired Services requires that federal departments submit formal five-year investment plans at a minimum of every three years and defines specific requirements for their content as well as the monitoring and reporting of investment planning. In consultation with TBS, Natural Resources Canada (NRCan) has further refined the definition of reportable investments included in the departmental investment plan, as follows:

- Valued at $1 million or more and allocated over a period of up to five years;

- Used for a non-recurring purchase (goods or services) with the expectation of a future return of value to NRCan such as an increase in outputs, revenue, or assets [quantitative value] or the acquisition of increased organizational capacity (knowledge, expertise, or training) [qualitative value]; and,

- Excluding activities related to daily operations and maintenance (e.g., eTool post-implementation training, roof replacement of a laboratory facility), liability obligations (e.g., environmental assessment conducted in compliance with regulations, such as the Canadian Environmental Assessment Act, to reduce risks to the environment), and unplanned funding pressures (e.g., program risks resulting from the impact of budget constraints).

NRCan’s formal departmental investment plan is prepared and updated by the Investment Planning Office, within the Corporate Management and Services Sector (CMSS), with input from Sector planning offices. Departmental oversight is provided by the Investment Review Board (IRB) which serves as the senior management advisory committee responsible for assessing Sector investments and investment portfolios, and making recommendations on priorities for the review and approval of the Deputy Head. The role of the IRB is performed by the Planning and Reporting Committee (PRC), which is co-chaired by the ADM of CMSS and the ADM of the Strategic Policy and Results Sector (SPRS), and has Director General-level membership from all Sectors as well as functional areas within the Department.

NRCan has prepared three investment plans under the TBS Policy Framework. The previous investment plan covering the five-year period from 2013-14 to 2017-18 included $1,448 million in planned spending on reportable investments. The current departmental investment plan covers the period from 2016-17 to 2020-21 and includes $237.8 million in planned spending on reportable investments. Most of the decrease is attributed to: investments that were completed, the transfer of responsibilities for Port Granby and Port Hope to Atomic Energy of Canada Limited, and the refining of NRCan’s definition of a reportable investment. In 2015-16 a five year capital asset plan (2016-17 to 2020-21) was also developed to capture the Department’s existing capital assets and highlight future asset needs. NRCan’s Vote 5 capital spending authority for 2016-17 is $53.3 million. The current plan was submitted to TBS for feedback in October 2016.

Text version

This figure illustrates the distribution by category of the ongoing and future reportable investments included in NRCan’s 2016-17 to 2020-21 investment plan, valued at a total of $237.8 million. The distribution of reportable investments is as follows: $140.3 million for investments in real property, $60.5 million for investments in Science & Technology, $34.4 million for investments in Information Technology, and the remaining $2.6 million for ‘other’ investments that do not fall into any of the other categories.

The Audit of Investment planning was approved by the Deputy Minister as part of the Risk-Based Audit Plan for 2016-2017.

AUDIT PURPOSE AND OBJECTIVES

The objective of this audit was to assess the management control framework and processes in place to support the development of the departmental investment plan.

Specifically, the audit assessed whether:

- An adequate governance structure and related governance mechanisms have been established to support departmental investment planning;

- Adequate processes have been established to support the development of the departmental investment plan, in compliance with TBS guidance and in alignment with the strategic objectives and priorities of the Department; and,

- An adequate monitoring and reporting framework has been established that enables decision making and measures the implementation of the departmental investment plan.

AUDIT CONSIDERATIONS

A risk-based approach was used in establishing the objective, scope, and approach for this audit engagement. A summary of the key underlying areas of risk taken into consideration includes the following:

- The governance framework may not support an integrated departmental approach to investment planning and the development of the investment plan;

- Investment planning processes may not be integrated with related strategic, business, and financial planning activities (i.e. IT Investment Planning, Capital Asset Plan, etc.) to ensure alignment of resource allocation management with the strategic objectives and priorities of the Department;

- Communication, guidance, and tools may not support the development of the investment plan; and,

- A framework may not have been established to monitor and report on the implementation of the approved departmental investment plan and enable decision making.

SCOPE

The scope of the audit included a review of the approved departmental investment plan for 2016-17 to 2020-21 as well as the investment planning processes and monitoring and reporting practices in place to support the development of the plan.

The audit focused on investment planning and not on project management; therefore, the scope of the audit did not include project planning, project execution, project close-out, or post project review. An audit of project management is included in the Risk-Based Audit Plan for fiscal year 2018-19.

APPROACH AND METHODOLOGY

The audit was conducted in accordance with the TBS Policy on Internal Audit and the Government of Canada’s Internal Auditing Standards and entailed the following:

- Reviewing relevant policy instruments and business processes;

- Reviewing key documents and relevant background information, including previous audit reports relating to investment activities;

- Conducting interviews with key personnel and members of departmental governance bodies; and,

- Considering relevant audits performed by other federal departments.

The conduct phase of this audit was substantially completed in September 2016.

CRITERIA

The criteria were developed primarily from the TBS Policy on Investment Planning – Assets and Acquired Services. The criteria guided the fieldwork and formed the basis for the overall audit conclusion. Please refer to Appendix A for the detailed audit criteria.

FINDINGS AND RECOMMENDATIONS

GOVERNANCE STRUCTURES AND MECHANISMS

Summary Finding

Governance structures have been established to support departmental investment planning, with the intent of providing centralized oversight to an otherwise decentralized process. Roles, responsibilities and accountabilities of the parties involved in investment planning and the development of the investment plan have not been clearly defined, and communicated to ensure they are generally understood.

The audit identified opportunities to improve the current monitoring and reporting framework and supporting guidance to enable decision making and measure the implementation of the departmental investment plan.

Supporting Observations

An adequate governance structure allows for management to exercise oversight and enables the achievement of departmental objectives and priorities through regular monitoring and reporting. The audit sought to determine whether the investment planning governance structures provide leadership, oversight, and a challenge function supporting the alignment of reportable investments with departmental priorities; and whether there is clarity of roles, responsibilitiesand accountabilities. The audit also examined whether an adequate monitoring and reporting framework has been established that enables decision making and measures the implementation of the departmental investment plan.

Roles, Responsibilities and Accountabilities

The Deputy Minister is supported in the role of Investment Approval Authority by the Investment Review Board (IRB) and the Investment Planning Office (IPO). This role is also supported by Sector Assistant Deputy Ministers (ADMs), as Investment Sponsors responsible for prioritizing and approving proposed reportable investments within their respective Sectors.

The IPO is responsible to: lead the production of the departmental investment plan for centralized reporting to TBS; develop and maintain planning and reporting tools related to investment and project management; and oversee the planning and reporting cycle to ensure integration, continuous improvement, and policy compliance. In addition, the IPO assembles information provided by Sector Planning Officers and various other planning processes to support centralized monitoring and reporting.

Given that most investment planning activities are decentralized and occur at the Sector level, the IRB was created with the intent of providing a centralized oversight function for departmental investment planning. The IRB, supported by the IPO, is mandated to serve as “the senior management advisory committee responsible for assessing Sector investments and investment portfolios, and making recommendations on priorities for the review and approval of the Investment Approval Authority”. The role of IRB is performed by the NRCan Planning and Reporting Committee (PRC) which is co-chaired by the ADM Corporate Management and Services Sector and the ADM of the Strategic Policy and Results Sector, and includes Director General-level membership from all Sectors and functional areas.

The PRC’s Terms of Reference lists one of its mandates as that of "undertaking the roles and responsibilities of the IRB, as established in the NRCan Investment Planning Framework (NIPF)”; however, this document does not make any reference to the IRB's Terms of Reference, which is a separate document. The IRB's Terms of Reference have not been reviewed since 2013, and includes references to documents and processes that are not currently in use, including the NIPF and review of quarterly Investment Dashboards. Interviews with committee members confirmed that roles and responsibilities of the IRB may not be well understood.

Monitoring and Reporting

Regular reporting provides governance bodies with information they require to ensure effective oversight of projects and prioritize investment decisions. Monitoring the progress of investments is critical to ensuring the continuous improvement of processes and sound stewardship of resources.

In December 2014, the IPO prepared the first ‘Annual Report on the NRCan Investment Plan 2013-14 to 2017-18’ for the Deputy Minister, NRCan’s investment approval authority. The report summarized the results achieved for the period and the current status of reportable investments, and is intended to show accountability and sound investment management practices. This report was not produced as required under the current investment plan in 2015-16, due to competing priorities. The annual report is not required to be produced in 2016-17 as this is the year of production of the new investment plan.

Projects valued at $1 million or more are monitored under the Project Management Framework and reported on a quarterly basis to the Deputy Minister. The IPO updates and validates reportable investments with Sector Planners and Sector Financial Advisors on a quarterly basis, and assembles the information into reports intended for IRB review. The audit was unable to confirm in the minutes that these reports had been distributed to IRB members, or that they were discussed during meetings.

Oversight and Challenge Function

The PRC undertakes the roles and responsibilities of the IRB twice a year during the PRC’s regular bi-monthly meetings, and, as a result, IRB minutes are a subset of the PRC’s minutes. The audit review of PRC meeting agendas and minutes did not identify the Committee exercising a challenge function regarding monitoring and reporting on the progress of investments. Interviews conducted with IRB members concurred with this assessment.

One of the additional responsibilities of the IRB is to review funding requests from the Sectors related to emerging or critical needs that are not otherwise budgeted for, and to make recommendations to the Deputy Minister for final approval. This process accommodates all types of activities, presenting the inherent challenge of developing criteria that are consistent to encompass the wide variety of investments. In the current era of fiscal restraint, informed decision-making is essential to the prioritization of limited resources. As each Sector follows its own approach to determine its priority investments, this introduces inconsistencies in the prioritization process from Sector to Sector even before a funding request is submitted to the IRB. Each funding request submitted to the IRB for endorsement follows a prescribed format; and priority determination criteria and processes have been created for the IRB to evaluate funding requests that encompass five broad assessment criteria ranging from ‘highly recommend’ to ‘not recommend’. IRB members indicated that they were not adequately supported with guidance on the criteria and supporting documentation to assess funding requests. IRB members also indicated that the results of the prioritization exercise and final approval of funding requests were not well communicated to them.

RISK AND IMPACT

The governance framework may not support monitoring of an integrated departmental approach to investment planning if roles and responsibilities for monitoring and reporting, processes to guide decision making, and regular reporting are not clearly defined and effectively communicated to members of oversight bodies.

RECOMMENDATIONS

- The Assistant Deputy Minister Corporate Management Services Sector (ADM CMSS) and ADM Strategic Policy and Results Sector (SPRS), as co-chairs of the Investment Review Board (IRB), should ensure that the roles and responsibilities of the IRB are clearly defined and communicated to new and continuing Planning and Reporting Committee (PRC) members, in fulfilling the role of the IRB for the regular monitoring of reportable investments.

- The ADM CMSS should ensure that the IRB members are well supported and informed with respect to the prioritization process and criteria to be applied in support of funding recommendations; and that the rationale supporting the final decision is communicated to IRB members.

MANAGEMENT RESPONSE AND ACTION PLAN

Management agrees. In response to recommendation 1:

The Co-Chairs of IRB will update the IRB Terms of Reference and circulate to IRB members.

The ADM SPRS, as secretariat for the IRB, will update the IRB members list and ensure when new members join, that they are provided with the Terms of Reference. In addition, the forward agenda for PRC will include monitoring of Reportable Investments.

Position Responsible: ADM CMSS and ADM SPRS

Timing: March 31, 2017

Management agrees. In response to recommendation 2:

In preparation for 2017-18 internal funding requests, the ADM CMSS will implement process improvements, including updating rating criteria to facilitate the accurate prioritization funding requests. The ADM CMSS will also implement measures to improve transparency around decision making by communicating DM funding decisions and rationales to IRB members.

Position Responsible: ADM CMSS

Timing: March 31, 2017

INVESTMENT PLAN AND SUPPORTING PROCESSES

Summary Finding

Lessons learned through the development of the previous investment plan have been incorporated into efforts to streamline the current investment planning process, including leveraging several related planning exercises. Additional opportunities were identified to further integrate the development of the investment plan with related corporate planning activities, such as the capital asset plan.

The five-year departmental investment plan was renewed within the three-year scheduled timeframe. In addition, it was circulated to Sector ADMs and IRB members for feedback before submission to the TBS in October 2016. The audit identified gaps in the information presented in the current investment plan as compared to TBS guidance, including risk management and performance measurement.

Supporting Observations

As per the TBS Policy on Investment Planning – Assets and Acquired Services, effective investment planning should ensure that resources are “allocated in a manner that clearly supports program outcomes and government priorities.” The audit sought to determine whether adequate processes have been established to support the development of the departmental investment plan, in compliance with TBS guidance and in alignment with the strategic objectives and priorities of the Department.

Investment Planning Processes

The Investment Planning Office (IPO) has implemented a number of practices that have generally reduced duplication of effort and lessened some of the burden on Sectors associated with providing similar data through multiple processes. On an annual basis, to support monitoring and reporting, the IPO verifies and updates the departmental reportable investment list of assets and acquired services in consultation with the Sectors. In addition, validation templates are also sent by the IPO to the Sectors’ planners or their Sector Financial Advisor during two of the other quarters to request updates on the progress of reportable investments. In an effort to further integrate investment planning into existing reporting mechanisms, the IPO obtains data and progress validation for all reportable investments monitored as projects through the Project Management Office.

As a result of the streamlined approach that was implemented by the IPO after the previous plan, the definition of a ‘reportable investment’ was refined such that the number of investments requiring monitoring and reporting decreased from 44 to nine. There are 13 reportable investments under the current plan. Any investments listed in the previous investment plan that did not meet the new NRCan-adapted reportable investment definition remain under the responsibility of the Investment Sponsor and are no longer monitored or reported on under the departmental Investment Planning and Project Management processes.

To support lessons learned from the first investment plan, the departmental Executive Committee approved the NRCan Investment Planning Framework (NIPF) in 2012 to serve as the implementation structure for the departmental investment plan. The 2016-17 to 2020-21 Investment Plan also includes a reference to the NIPF. The audit found that this framework was not used during the development of the new plan; however, the IPO developed a streamlined process that was presented to both the IRB and the Executive Committee in 2014. Under this streamlined process the IPO has developed tools, including standardized templates and supporting guidance, for the development and monitoring of the departmental investment plan.

Integration with Related Planning Exercises

The IPO has attempted to structure its planning cycle to align with other planning exercises such as the development of departmental Information Technology (IT) and real property plans; the annual procurement plan was also a source of data for future requirements in services. Nevertheless, the audit identified opportunities to further align the timing of validating information on new investments categorised under assets and acquired services to their departmental planning cycle, in particular the capital asset plan. The capital asset plan was first created in 2015-16, at the request of the former Deputy Minister; there had been no formal department-wide capital asset plan prior to this exercise. The capital asset plan is intended to provide information on the status of existing capital assets and assets in the process of being developed or acquired; it also presents an analysis of the next five years by focusing on priority needs which are considered essential to the continuous delivery of NRCan programs and services. In this plan it is acknowledged that as a department, there is not a common understanding of the role that this plan could play in terms of investment management decisions. The IPO was responsible for preparing this plan, through consultation with Sector planning offices.

The Investment Plan

The audit reviewed the current draft investment plan against the TBS Policy on Investment Planning – Assets and Acquired Services and the TBS Guide to Investment Planning – Assets and Acquired Services and observed some information gaps and inconsistencies, as described below.

The 2016-17 to 2020-21 Investment Plan includes the following categories for ongoing and future investments: Science & Technology, Real Property, IT, and Other. Although the plan has clearly captured the Department’s planned reportable investments that are projects over the next five years, it includes only three years of information for both IT and S&T, and there is a general time frame indicated for the spending on real property investments that relates to the Federal Infrastructure Initiative. Sector Planning Officers noted that it was difficult to project or plan beyond three years. The plan also includes information on investments that are not subject to monitoring under the reportable investment framework and are overseen by separate governance committees and processes. Although there is nothing in the policy guidance that would preclude this information from being added, there is no explanation in the plan as to why this information has been included.

The TBS Policy on Investment Planning – Assets and Acquired Services notes that effective investment planning underpins a department's ability to manage investments of highest priority and greatest risk to the government. As such the policy requires that the investment plan include an explanation of the department’s risk management approach to investment planning including: the identification of areas of greatest risk to program integrity, risk mitigation strategies and residual risk. The audit noted that this level of detail was not included in the current plan. The policy also describes one of the key elements of effective management of investment planning as ensuring appropriate, ongoing measurement of investment performance. The TBS Guide on Investment Planning-Assets and Acquired Services requires that investment plans include a description of key performance indicators and evaluation processes including evaluation of the previous planning cycle and a description of the methodology used for measuring the achievement of investment planning. This information was not captured in the current investment plan.

RISK AND IMPACT

Investment planning processes may not be appropriately integrated with related strategic, business, and financial planning activities to ensure compliance with TBS guidance and to support alignment of resource allocation management with the strategic objectives and priorities of the Department.

RECOMMENDATIONS

- The Assistant Deputy Minister Corporate Management Services Sector (ADM CMSS), in consultation with the Investment Review Board (IRB), should take steps to address identified gaps in the departmental investment plan to support compliance with TBS guidance.

- The ADM CMSS, in consultation with the IRB, should consider creating clear linkages between the capital asset plan and the investment plan to ensure a higher level of integration between departmental capital asset and investment needs.

MANAGEMENT RESPONSE AND ACTION PLAN

Management agrees. In response to recommendation 3:

To support compliance with TBS Guidance, the NRCan Investment Planning Office will address the gaps identified in the draft departmental Investment Plan by Audit and TBS, and submit to TBS through the TB Submission. This recommendation will be deemed fully implemented upon TBS approval of the TB Submission.

Position Responsible: ADM CMSS

Timing: January 2017 – this deadline is dependent on TBS timeframes, which are outside of NRCan control, and could shift

Management agrees. In response to recommendation 4:

The NRCan Investment Planning Office will improve linkages between the Capital Asset plan and the Investment Plan by including information on the capital assets inventory in investment planning reports presented to the IRB as the investment planning governance entity.

Position Responsible: ADM CMSS

Timing: March 31, 2017

APPENDIX A – AUDIT CRITERIA

This audit assessed the management control framework and processes in place to support the development of the departmental investment plan.

The following audit criteria were developed primarily from the TBS Policy on Investment Planning – Assets and Acquired Services and were used to conduct the audit:

| Audit Sub-Objectives | Audit Criteria |

|---|---|

| Audit Sub-Objective 1: To determine whether an adequate governance structure and related governance mechanisms have been established to support departmental investment planning. | 1.1 Governance structures and mechanisms provide leadership, oversight, and a challenge function to support alignment of investments with departmental priorities. |

| 1.2 Roles, responsibilities, and accountabilities of parties involved in investment planning and the development of the investment plan are clearly defined, communicated, and understood. | |

| Audit Sub-Objective 2: To determine whether adequate processes have been established to support the development of the departmental investment plan, in compliance with TBS guidance and in alignment with the strategic objectives and priorities of the Department. | 2.1 Investment planning processes are appropriately integrated with related departmental planning processes (i.e. IT Investment Planning, Capital Asset Plan, etc.) to support the alignment of resource allocation management with the strategic objectives and priorities of the Department. |

| 2.2 Appropriate tools and guidance to support investment planning have been developed and communicated to all stakeholders. | |

| 2.3 The departmental investment plan and supporting processes reflect the guidance of the TBS policy suite. | |

| Audit Sub-Objective 3:To determine whether an adequate monitoring and reporting framework has been established that enables decision making and measures the effectiveness of the departmental investment plan. | 3.1 A framework has been established to monitor the implementation of the departmental investment plan and to support the continuous improvement of investment planning processes. |

| 3.2 Actual performance of the departmental investment plan is regularly reported to senior management and reviewed against expected results to inform decision making. |

Page details

- Date modified: